ODD · AI · Data Infrastructure · A DiligenceVault Perspective

What AI Changes

About the DDQ -

and What

It Doesn't

DDQs are not going away. The case for them, built on attestation, transparency, and regulation, is stronger than ever. What is changing is how they are deployed: what they cover, how often, and how much of their current weight can be carried by a connected data layer. The diligence professionals who run these processes, and the managers who maintain high-quality disclosure, are the reason this conversation is worth having.

- →DDQs remain essential. Attestation, transparency requirements, and regulatory expectations mean the manager's direct, accountable statement cannot be replaced by any data source.

- →A standard data layer answers factual questions before the DDQ is sent, compressing time for both sides without reducing quality, and improving ongoing monitoring.

- →DDQ utility varies by context. Smaller managers, lower-transparency markets, and new relationships warrant fuller questionnaires. Established relationships with connected data warrant focused attestation.

- →AI-generated DDQ responses mean the quality of writing is no longer a signal of the underlying practice, shifting the verification burden toward independent confirmation and in-person review.

- →The DDQ isn't shrinking because it's asking less. It's becoming more precise because the data layer handles what it can handle, leaving attestation for what only a manager can answer.

Why DDQs Are Here to Stay

Market research is clear on this: DDQs are not going away. Three forces make them durable, and none of them is weakening.

Attestation. A manager's direct, accountable statement about their operations, governance, and investment processes cannot be replicated by any data source, extraction model, or third-party verification. When a manager answers a question about their valuation process or their approach to conflicts of interest, they are making a deliberate statement. The framing is theirs. They are on record. That doesn't guarantee accuracy, but it creates intent and liability in a way no document does. It also reveals something documents never convey: how the manager thinks. Tone. Framing. Defensiveness versus clarity. These are signals that belong to attestation alone.

Transparency. The DDQ is one of the few structured mechanisms in asset management for ensuring that managers articulate their own operations directly. Transparency has improved materially over the past decade, but it is not uniform. Smaller managers, private markets vehicles, newer fund structures, and less institutionalized platforms operate in environments where the DDQ remains the primary disclosure mechanism. In these contexts, the questionnaire is not redundant. It is the first structured conversation the allocator and manager have about how the firm actually works.

Regulation. Regulatory expectations around documented governance, operational controls, and compliance programs require structured, manager-provided responses. The SEC's examination priorities increasingly focus on whether firms can demonstrate, not just assert, that their stated policies reflect actual practice. The DDQ creates the documented baseline that makes that demonstration possible. As regulatory scrutiny of AI usage, off-channel communications, and valuation practices intensifies, the manager's own attestation to their controls becomes more important, not less.

The DDQ today is being asked to do a new job, which is different from the job it has accumulated over twenty years of scope creep.

It is worth being direct about something before going further. The diligence practitioners who design questionnaires, conduct onsite visits, review documentation, and make the judgment calls that protect their investments and investors - are doing serious and skilled work. The same is true of the managers who invest in maintaining high-quality disclosure materials, answer questions thoroughly, and treat the diligence process as a genuine conversation rather than a compliance exercise. The argument in this article is that the infrastructure available to support that work is improving, and that improvement changes what is possible, not what is valued.

Attestation vs. Extraction: Not the Same Thing

Two distinct things are happening in diligence right now. They look similar. They are fundamentally different.

Manager attestation is a direct, accountable statement. The manager is on record. It creates intent and liability, and captures the qualitative signals, tone, framing, how a manager characterizes uncertainty, that no document conveys.

AI extraction reflects what a source document says. Documents, PPMs, LPAs, fund agreements, are legal and structural artifacts drafted to limit liability and expand the scope of possibilities for the GP, they describe what is permissible, not necessarily what is current practice. A control that exists in writing but not in practice still gets extracted as fact. And when a document is wrong, that error gets scaled.

Extraction is genuinely useful, not as a substitute for attestation, but as a check against it. The hybrid is not a compromise between two approaches. It is a more rigorous design than either one alone.

What Actually Needs Attestation

The DDQ covers a wide range of questions, service providers, regulatory status, operational controls, governance structures, investment processes. Not all of these require the same thing from the manager. Some confirm a factual record. Others ask the manager to articulate something that only they can describe, how decisions are made, what happens under stress, where the real governance tensions lie. The DDQ's deepest value is in the second category. These are the questions that require a human to stand behind the answer, and they are the ones that become more revealing when the DDQ isn't crowded with questions that documentation or data can more efficiently address.

What the DDQ is uniquely positioned to surface

The DDQ's distinctive value is in the questions that cannot be answered by a document, a database, or any data feed, the questions that require a human to articulate something and stand behind the answer. These are questions about judgment, governance, and how the firm actually operates under conditions that haven't been written down anywhere.

Why these questions matter , live examples

Thoma Bravo announced in April 2026 that it would wind down its growth equity strategy and not raise another vehicle. The trigger: both co-heads of the growth business had departed. A $183 billion firm with deep bench strength across its buyout practice found that the departure of the two people who built and ran a specific strategy was effectively the end of that strategy.

A key person clause in an LPA describes what happens contractually when a named individual leaves. It does not describe whether the strategy survives, whether the institutional relationships, sourcing network, and investment judgment are tied to the person or to the firm. The question "walk me through how this strategy continues if either of you leaves" is an attestation question. No extraction model pulls that answer from a PPM.

In Q1 2026, multiple large private credit interval funds faced redemption requests significantly above their base quarterly thresholds. Cliffwater's $33 billion fund received requests totalling approximately 14% of shares and capped at 7%. Blackstone's BCRED received 7.9% requests and deployed $400 million from the firm to help meet them. Ares capped at 5% after requests of 11.6%. BlackRock capped at 5% after requests approached twice that level.

The gates functioned as designed. That is not the point. The question is whether allocators who had capital in these vehicles understood, before the stress event, what the decision-making process looked like when redemptions exceeded the fund's base threshold. Who decides between a 5% and 7% cap. How investors are prioritized. What the communication protocol is. Whether the manager had stress-tested these mechanics.

None of those answers live in the fund documents. The LPA describes the gate mechanism. It does not describe the governance of it under pressure.

The DDQ as a Precision Instrument, Not a Universal Process

Consider what it means to run diligence across a portfolio of five hundred managers. Manually piecing together operational information from different document formats, disclosure styles, and information sources, without a consistent structure, is not a viable process at that scale. The DDQ exists precisely because consistency matters. It creates a common language across managers, a baseline that makes comparison possible, and a structured record that gives monitoring its reference point over time. That is not a problem to be solved. It is the DDQ's core function.

What varies is how that function is best served given different contexts. Manager size, transparency level, regional norms, relationship maturity, and strategy type all shape what the DDQ should cover and how much it should ask. An allocator reviewing a new relationship with a smaller, private markets manager needs a different instrument than one conducting an annual review of a large, well-documented platform where significant disclosure infrastructure already exists. Applying the same template to both, without calibration, misses what makes the DDQ valuable and amplifies the parts that slow everyone down.

Size matters

Smaller managers often send full policies. Larger managers typically send summaries. Neither is inherently more useful, but they represent different information environments. A smaller manager's full policy document may be the most direct window available into how they actually operate. A larger manager's summary may be highly curated and require deeper follow-up to get beneath the surface. The DDQ design should reflect this: for a new relationship with a smaller manager in a lower-transparency environment, a comprehensive questionnaire is the right starting point. For a large, well-documented manager with an established data-sharing relationship, the DDQ should focus on the questions that haven't already been answered.

Regional context shapes what's needed

INREV DDQs, for example, are weighted more heavily toward investment due diligence than operational due diligence. This reflects a deliberate design choice by INREV as a standards body, real estate as an asset class has investment-specific metrics, valuations, occupancy data, and sector exposure that dominate the diligence conversation, and INREV's frameworks have evolved to prioritize that depth. The ODD layer is relatively thinner by design, not because operational information is handled through other structured channels. It is a useful illustration of how a standards body can deliberately calibrate the scope of a DDQ to the information that matters most for a given asset class and investor community.

Transparency level is the critical variable

DDQs are most necessary when transparency is lowest. In markets, strategies, or manager relationships where direct disclosure is the primary mechanism for operational information, the questionnaire is doing essential work. As transparency improves, through better data infrastructure, stronger regulatory disclosure requirements, and more developed LP-GP relationships, the questionnaire can be progressively focused on what remains opaque. Managers are generally more transparent than they were a decade ago. The DDQ should adapt to reflect that, rather than applying a fixed template regardless of what's already known.

What managers actually want from standardization

Managers have told us directly: there will never be a single universal DDQ standard, and most have accepted that. But managers would benefit significantly from standardization of at least part of the dataset, the operational facts, the service provider network, the regulatory record, the governance structure. Maintained in one place, that layer would allow managers to direct their attention toward the questions that genuinely require it, rather than re-entering the same foundational information across dozens of questionnaires. That reduction in repetitive burden would improve the quality of what managers provide, not reduce it.

The internal DDQ model

One approach gaining traction among allocators with more concentrated or smaller portfolios: answer the DDQ internally first. Work through each question against existing data sources before sending anything to the manager. Some questions will already be answered. A smaller set will need direct manager input. Five questions you want answered before a meeting. Ten you want the manager to check and attest to. What arrives in the manager's inbox is a focused set of genuine questions, not a comprehensive template, and the conversation that follows is more revealing for it.

That baseline function is one of the DDQ's most important and least discussed roles. When you are monitoring five hundred managers, the ability to compare how a manager answers a specific question today versus two years ago, and against how others in the same strategy answer it, is the foundation of meaningful monitoring. It is also what makes drift visible: when a manager who previously answered a governance question with specificity begins answering it with generalities, that change is itself a signal. Losing that baseline in the name of efficiency would be a significant step backward. What a data layer enables is not the elimination of the baseline, it is the compression of the time and effort required to maintain it.

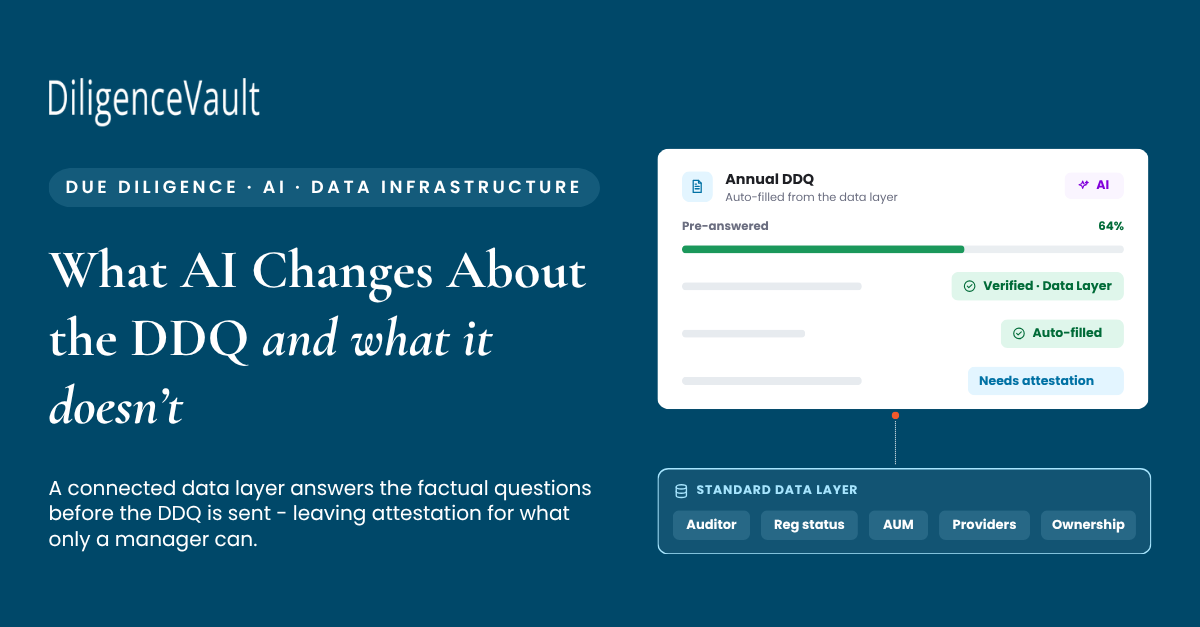

What a Standard Data Layer Changes

A DDQ deployed as an annual uniform process, the same questions, the same format, regardless of what is already known about a manager, carries an embedded cost that compounds across every relationship in a portfolio. The answer is not to eliminate the cycle. It is to build the data layer that should have existed underneath it, so that each cycle can focus on what it was always meant to surface.

A natural question follows: if databases already capture much of this information, regulatory filings, fund administrator records, background screening, why does the DDQ still ask for it?

Three reasons, and they are not going away. First, no database covers the full universe an allocator might be tracking. The manager in a less-covered market, the newer fund, the strategy that sits outside the main indices, these are often exactly the relationships where operational diligence matters most and where third-party data coverage is thinnest. Second, database records go stale. A fund administrator change, a regulatory amendment, a key person departure, these updates reach different databases at different speeds, and sometimes not at all. Third, fragmented sources create fragmented pictures. Cross-referencing five different databases to assemble a view of one manager, multiplied across hundreds of relationships, is neither efficient nor reliable. What allocators actually need is a single source of truth, structured, current, manager-confirmed, and consistent across every manager in the portfolio.

That is what the DDQ provides that databases do not: a direct line to the manager, a structured format that enables comparison, and a record of how the manager has characterized their own operations over time. The question is not whether to collect this information, it is how to collect it in a way that is current, consistent, and proportionate to the diligence it enables. A standard data layer does not replace the DDQ's role here. It upgrades it, from a periodic self-report to a maintained, structured, permissioned record that an allocator can trust across the full depth of their portfolio.

A standard data layer changes the DDQ in three specific ways.

This is not a reduction in diligence. It is an improvement in how diligence resources are allocated. The allocator who has pre-answered the factual layer does not ask a manager about their auditor in a quarterly check-in. They already know. The question they ask is what changed in the audit process since last year, and why.

DiligenceVault's Blaze Data Layer is an industry-wide initiative built on exactly this premise. Rather than treating the data layer as a problem each allocator-manager pair solves independently, Blaze establishes a standardized set of operational data fields, service providers, AUM, fund structure, governance, personnel, that managers maintain in one place and share, with permission, across any allocator relationship. It is not a DDQ replacement. It is the structured foundation that makes the DDQ do its actual job. A manager who maintains their Blaze record is not filling out a questionnaire for each allocator, they are maintaining a single source of truth that any permissioned allocator can access, confident that the data is current, structured, and manager-confirmed. The time saved on repetitive data entry is time recovered for the conversations that matter. And for the industry as a whole, a shared standardized layer means that allocators monitoring hundreds of managers are working from a consistent dataset, not a patchwork of self-reported formats that vary in currency, completeness, and structure.

The Complication AI Creates

There are two AI dynamics now shaping the DDQ conversation, and they pull in opposite directions. The first is well-discussed: managers using AI to generate DDQ responses. The second is less discussed but equally important, allocators using AI to extract information from documents rather than requesting it from managers directly. Both change the verification calculus, and understanding them together matters.

On the extraction side: AI can surface information from PPMs, fund agreements, and offering memoranda quickly and at scale. But extraction shifts the burden of review onto the allocator. Instead of the manager confirming and attesting to their current operational facts, the allocator is now responsible for interpreting what a document says, assessing whether it is current, and deciding whether it accurately reflects practice. That is more work for the allocator, not less, and it removes the manager's accountability from the process. The DDQ, properly used, puts that accountability back where it belongs: with the manager, on the record.

Manager's AI-generated responses, on the other hand, speeds up the process without shifting the burden, provided the AI is working from the manager's own structured data rather than generating answers from scratch. A manager using AI to autofill a DDQ from their maintained operational record is doing something genuinely useful: reducing the time spent on repetitive data entry while keeping the manager as the source and the attestor. That is the model that works. The problem arises when AI is used to generate answers that have no operational grounding at all.

A few managers are using AI to generate DDQ responses from minimal context. Give an AI a strategy description and a prompt to align with industry best practices. The results are striking. The policies read well. The responses sound considered. The language is professional and complete. Most of it does not reflect what the manager actually does.

When a well-crafted DDQ response requires no operational knowledge to produce, the quality of the written response is no longer a signal of the underlying practice. An allocator cannot infer from polished writing about risk controls or succession planning that those controls or that planning actually exists. The written DDQ stops being evidence and becomes a starting point, a set of claims that requires independent verification before it means anything.

This is precisely what ODD practitioners described at GAIM Ops Cayman in April 2026: returning to in-person site visits specifically because AI-generated documentation is indistinguishable from documentation that reflects operational reality. The only reliable check, in that environment, is being physically present with the people and systems in question.

AI making the written DDQ easier to produce accelerates the return to human verification. The irony is exact.

A standard data layer is part of the answer here too. Manager-provided structured data through a permissioned platform has provenance, it comes from the manager's own record, it is timestamped, it is auditable over time. It is fundamentally different from a well-written response to a question. The data layer does not replace verification. But it creates a baseline against which AI-generated narrative responses can be checked, and a record of consistency or inconsistency over time that no single DDQ response can provide.

This points to what is perhaps the most underappreciated argument for the structured data layer: it is the prerequisite for AI to do useful work in diligence at all. AI models generate meaningful signal when they operate on structured, consistent, longitudinal data. A time-series of a manager's operational disclosures, service providers, AUM, personnel, governance structure, attestations, collected in a standardized format across years, is the kind of dataset that allows AI to detect drift, flag anomalies, and surface patterns that no human reviewer monitoring hundreds of relationships could catch manually. A DDQ response from 2024 sitting in a PDF, a different response from 2022 in a spreadsheet, and a third from 2026 in a different format, that is not a dataset. It is an archive. The difference between the two is what determines whether AI can actually be applied to diligence at scale, or whether it remains a tool for processing one document at a time.

The Design Question

The DDQ is not going away. Three forces, attestation, transparency, and regulation, ensure its durability. What is changing is how it is deployed, what it covers, and how much of its current surface area should be occupied by questions that a connected data layer can already answer.

The opportunity is not to replace the DDQ. It is to compress it to its essential function, the manager's direct, accountable articulation of how their firm operates, makes decisions, and governs itself, while building the data layer that handles everything else. When that data layer exists, the DDQ becomes shorter without becoming weaker. The manager's time is spent on the questions that require genuine thought. The allocator's time is spent on the answers that reveal something. And the ongoing monitoring that happens between DDQ cycles becomes continuous rather than periodic.

Oversight is not weakened by reducing what happens in the formal review cycle. It is strengthened by building the continuous infrastructure that makes the review cycle more valuable, and more honest. The future DDQ is more demanding, not because it asks more, but because everything it asks requires a genuine answer.

The diligence teams who build this well will spend less time collecting and more time understanding. That is the job the DDQ was always meant to support.

Frequently Asked Questions

DDQs, Attestation, and the Data Layer

Are DDQs going away in asset management due diligence?

No. Three forces make DDQs durable: attestation (manager accountability cannot be replicated by any data source), transparency requirements (many managers operate in environments where direct disclosure remains the primary mechanism), and regulation (documented governance and operational controls require structured, manager-provided responses). What is changing is how DDQs are deployed, not whether they are used.

What is the difference between manager attestation and AI extraction?

Manager attestation is a direct, accountable statement from the manager about their operations and governance. It creates intent and liability and reveals qualitative signals, tone, framing, how a manager characterizes uncertainty, that no document conveys. AI extraction pulls information from source documents such as PPMs, LPAs, and fund agreements. Documents are legal and structural artifacts drafted to limit liability and expand the scope of possibilities for the GP, they describe what is permissible, not necessarily what is current practice. Extraction is useful as a verification layer against attestation, not a substitute for it.

How does a standard data layer change how DDQs are used?

A standard data layer, covering service providers, regulatory status, fund performance, AUM, background, insurance, and ownership, means that many factual questions in a DDQ can be answered before the questionnaire is sent to the manager. This compresses the time required for both sides without losing quality. The DDQ itself focuses on the questions that genuinely require manager attestation: judgment, governance, decision-making under stress, succession, and conflict management.

Why do DDQs vary in usefulness across manager size and region?

DDQ utility varies significantly by context. Larger managers typically provide summaries; smaller managers often send full policies. Regional norms differ substantially. European frameworks such as INREV weight investment due diligence more heavily, a deliberate design choice reflecting the investment metrics and valuations central to real estate diligence, not a function of operational data being captured through other channels. In markets with lower baseline transparency, the DDQ may be the primary disclosure mechanism available. The appropriate DDQ approach should be calibrated to the transparency environment, manager size, and relationship maturity.

What are the risks of AI-generated DDQ responses?

AI can generate professional-sounding DDQ responses from minimal context. The quality of a written response is no longer a reliable signal of the underlying operational practice, when a polished answer requires no operational knowledge to produce, allocators cannot infer that the practice exists. This shifts the verification burden toward independent confirmation, direct service provider calls, and in-person review. A standard data layer provides provenance and a record of consistency over time that narrative DDQ responses cannot.