Across more than a dozen 2026 private markets outlooks, the message is broadly constructive. Liquidity is improving. Capital is available. Innovation continues.

But for allocators, that consensus still leaves an important question unresolved: are portfolios designed to consistently realize private market returns in a more complex operating environment?

Returns are becoming more dispersed. Liquidity is uneven. Product structures are evolving faster than governance frameworks. At the same time, allocator mandates are expanding – decisions are being made at greater speed, across more strategies and structures, with rising expectations around data, transparency, and the effective use of technology.

In this context, approaching 2026 primarily through return expectations alone may understate the structural work now required: re-examining portfolio construction, strengthening operational due diligence, and investing in the systems and processes that enable disciplined decision-making as private markets continue to evolve.

What the 2026 Outlooks Largely Agree On

Before focusing on implications, it’s useful to anchor on consensus. Across the outlooks, several themes consistently emerge:

- Liquidity is improving, but selectively – not uniformly. While outlooks are “constructive,” liquidity generation remains “muted” and is heavily reliant on non-traditional channels like continuation funds, which now account for nearly one-third of PE exits.

- Return dispersion is widening across private equity, private credit, and real assets.

- AI is shifting from hype to real-economy impact, particularly in infrastructure, power, and operational value creation.

- Private credit remains attractive, but underwriting quality and structure matter more than ever.

- Secondaries, GP-leds, and evergreen vehicles are no longer niche tools they are permanent features of the private markets ecosystem.

None of these points are controversial. What is contested is how allocators should respond.

Where Allocators Are Most Likely to Get It Wrong in 2026

1. Assuming Exit Recovery Solves Liquidity

Many outlooks point to reopening IPO and M&A markets. That may help – but it does not restore the old liquidity model.

Private markets are larger, assets are held longer, and ownership is more concentrated. Liquidity is increasingly delivered through secondaries, continuation vehicles, and structured solutions, not traditional exits alone.

Allocator implication:

Liquidity must be designed into the portfolio, not assumed from market recovery. Liquidity stress-testing – using DPI assumptions and delayed exit scenarios should become a standard portfolio management tool, not an afterthought. Allocators seeing bifurcations between platforms that can generate liquidity through multiple channels and those reliant on traditional exits alone

2. Treating Private Credit as “Safe Yield”

Private credit remains the most consistently favored asset class across 2026 outlooks. However, several managers caution that risk is migrating – from spreads tightening to structures, collateral complexity, and workout execution.

As private credit expands into asset-based lending, specialty finance, real estate debt, and credit secondaries, outcomes become increasingly manager-specific and operationally driven.

Allocator implication:

Private credit is no longer defensive by default. Allocators must prioritize managers with demonstrated restructuring, recovery, and covenant enforcement experience – not just attractive yield histories.

Allocators are not rotating away from credit; they are expected to rotate within credit, from spread compression toward optionality, flexibility, and the ability to provide liquidity when others cannot.

3. Over Concentrating AI Exposure

AI appears everywhere in the 2026 outlooks but not all AI exposure is created equal.

Some managers emphasize enterprise adoption, infrastructure demand, and productivity gains. Others warn about valuation concentration and bubble dynamics. Increasingly, AI affects multiple layers of private markets:

- Growth equity: enterprise adoption and workflow integration

- Infrastructure: power generation, data centers, and digital assets

- Private equity: automation, analytics, and operational efficiency

Allocator implication:

AI exposure should be diversified across asset classes, not concentrated in thematic funds. Valuation normalization risk should be explicitly underwritten, not assumed away.

4. Confusing Evergreen Access with Liquidity

Evergreen and semi-liquid vehicles are expanding rapidly, particularly in wealth-facing channels. While these structures improve access, they also introduce new risks around liquidity mismatch, valuation discretion, and investor behavior.

Allocator implication:

Evergreen vehicles are structures, not asset classes, and must be underwritten accordingly. Liquidity buffers, redemption mechanics, valuation governance, and the use of secondary sales all require scrutiny – especially in evergreen credit strategies.

What This Means for Portfolio Construction in 2026

Liquidity Becomes a Portfolio Design Variable

Allocators should think in terms of liquidity sleeves, not just asset classes, to better align assets and liabilities:

- Growth-oriented, long-duration capital: private equity and venture

- Liquidity-generating or smoothing strategies: private credit and secondaries

- Stabilizing assets with contracted cash flows: infrastructure and core real assets

This approach is not about reducing risk – it is about controlling how and when risk surfaces.

Dispersion Makes Manager Selection More Important Than Allocation

Across outlooks, the gap between top – and median-performing managers is expected to widen. Multiple expansion is no longer a reliable return driver; operational execution, pricing discipline, and governance dominate outcomes.

Manager research depth and selectivity matter more than ever.

Infrastructure Regains Strategic Importance

Infrastructure and real assets are increasingly framed as beneficiaries of powerful structural forces:

- AI-driven power demand

- Energy transition

- Digitalization

For allocators, infrastructure can serve as a portfolio stabilizer, offering durability and inflation linkage while still participating in long-term growth themes.

Recalibrating Return Expectations

The 2026 outlooks do not signal a retreat from private markets – but they do point to a recalibration:

- Median returns may compress.

- Top-quartile returns remain achievable.

- Realized outcomes depend on liquidity, execution, and governance.

Allocators should place greater emphasis on DPI, cash-flow volatility, and stress scenarios, alongside headline IRRs.

The missing layer isn’t what allocators are worried about – it’s how those concerns are changing allocation behavior, pacing, and expectations for managers.

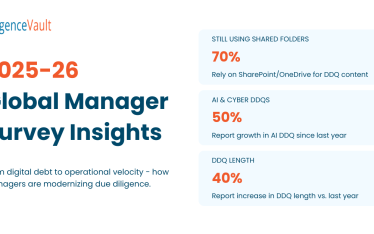

Operational Due Diligence: New & Expanded Focus Areas in 2026

In 2026, operational due diligence (ODD)will have new focus areas to help avoid operational failures, but also to preserve the conditions necessary for returns to be realized.

As private markets grow more complex through evergreen structures, expanded private credit, secondaries, and AI-enabled operations – ODD sits at the intersection of risk management, portfolio construction, and liquidity planning.

Click below to access the full framework and explore what allocators should actually do differently.