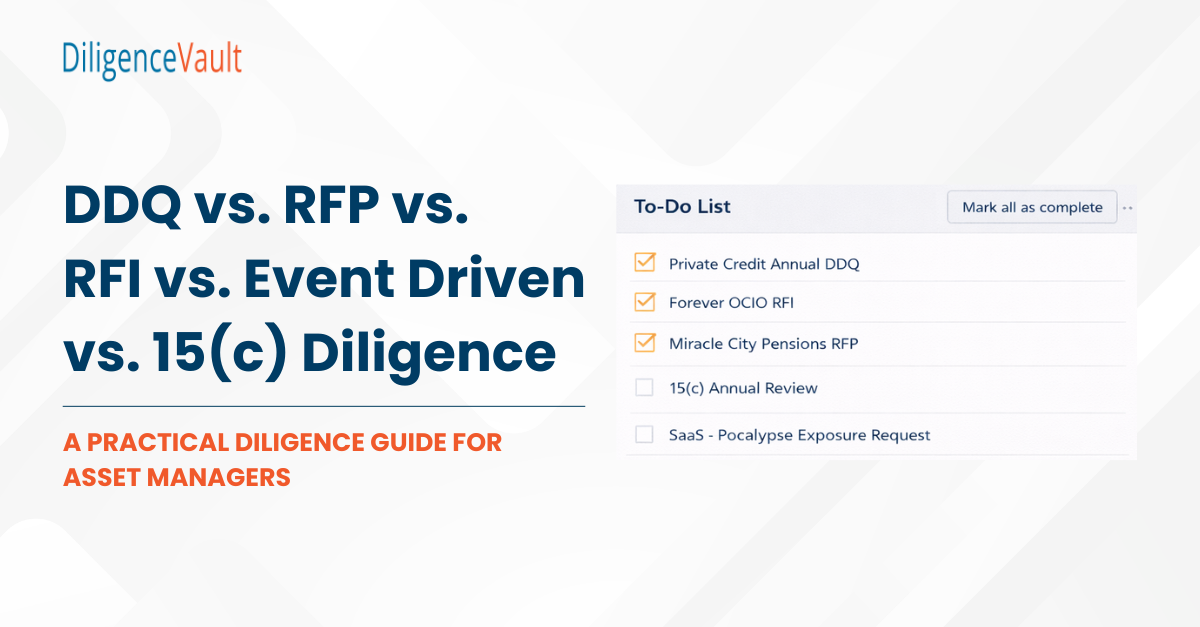

Asset managers are asked to complete DDQs, RFPs, RFIs, and 15(c) questionnaires every year. These documents often look similar: structured questions about strategy, performance, risk, operations, and fees.

But they are not interchangeable.

Each serves a distinct purpose in the investment lifecycle. Each carries a different level of regulatory and reputational risk. And each requires a different operational approach.

Understanding these differences is foundational to building a scalable, defensible diligence process.

What is the Difference Between a DDQ, RFP, RFI, and 15(c)?

At a high level, the distinction lies in intent:

- RFI (Request for Information) → Early-stage screening

- RFP (Request for Proposal) → Competitive mandate selection

- DDQ (Due Diligence Questionnaire) → Deep operational verification

- 15(c) Questionnaire → Statutory board approval under the Investment Company Act

While they often draw from overlapping data, they exist at different stages of the investor journey and require different levels of precision and control.

The RFI: Initial Screening and Positioning

An RFI is typically the first formal interaction in an institutional selection process. Consultants and allocators use RFIs to narrow a broad universe of managers into a shortlist.

RFIs are usually shorter and higher-level. They focus on strategy fit, performance track record, team structure, and high-level risk characteristics.

The risk level here is relatively low. However, inconsistencies introduced at this stage can resurface later. If an RFI describes AUM, performance attribution, or fee structures differently than a subsequent DDQ or RFP, it creates friction and credibility concerns.

The RFI sets the narrative foundation.

The RFP: Competitive Differentiation Under Pressure

An RFP is fundamentally different from an RFI. It is competitive, mandate-specific, and directly tied to winning new business.

RFPs require not only accurate information but contextual framing. Managers must explain how their process fits a specific mandate, benchmark, or portfolio objective. Responses are more narrative-driven and more customized.

This introduces a higher compliance risk. Tailored language can unintentionally create inconsistencies with prior disclosures. Marketing claims must align precisely with regulatory filings, DDQs, and performance reporting.

RFPs are where narrative meets governance.

The DDQ: Institutional Verification and Continuity

A DDQ is designed for deep operational due diligence. It is typically completed during manager onboarding and revisited annually or when material changes occur.

DDQs go beyond performance and positioning. They examine:

- Firm history, organizational structure, and ownership

- Risk management frameworks

- Compliance policies

- Trade controls and valuation processes

- AI, cybersecurity, and IT infrastructure

- ESG and DEI practices

- Service provider oversight

The defining feature of a DDQ is continuity. Answers must remain consistent over time. Changes are expected, but they must be intentional, documented, and explainable.

Unlike RFPs, DDQs are less about persuasion and more about verification. Increasingly, allocators are also turning operational due diligence (ODD) into a fundraising gatekeeper.

The 15(c) Questionnaire: Regulatory Accountability

The 15(c) questionnaire stands apart.

Required under Section 15(c) of the Investment Company Act, these materials support mutual fund board approvals of advisory contracts. They are highly structured, heavily reviewed, and often involve legal counsel.

15(c) responses focus on:

- Advisory fees and fee comparisons

- Services provided

- Performance versus peers and benchmarks

- Economies of scale

- Conflicts of interest

Historical consistency is critical. These materials form part of the regulatory record and may be scrutinized by boards and regulators.

15(c) is not a marketing exercise. It is a statutory obligation.

The Fifth Category: Event-Driven and Ad Hoc Diligence

Beyond formal RFIs, RFPs, DDQs, and 15(c) questionnaires, asset managers increasingly face event-driven and ad hoc diligence requests.

These are triggered by market events, regulatory developments, geopolitical tensions, or headline risk. They often require responses within hours, not weeks.

Examples include:

- Exposure to a specific issuer, sector, or region during market volatility

- Counterparty exposure to a distressed financial institution

- Liquidity or private credit exposure during stress events

- ESG controversies tied to a portfolio holding

- AI governance, cybersecurity posture, or operational resilience inquiries

Unlike scheduled DDQs or statutory 15(c) processes, event-driven diligence tests whether a firm’s internal data is accessible, current, and consistent across teams.

The risk is immediate and reputational. Delayed or conflicting responses during a market event can erode investor confidence quickly.

In volatile markets, responsiveness becomes a measure of institutional maturity.

Why Asset Managers Struggle With These Requests

Despite their differences, many firms manage RFIs, RFPs, DDQs, 15(c) questionnaires, and event-driven exposure requests in disconnected workflows.

Common challenges include:

- Information stored across spreadsheets, email threads, and shared drives – still used by nearly 70% of the managers

- Different teams maintain overlapping datasets

- Manual copy-paste from prior submissions

- Limited version control or historical tracking

- Scrambling to aggregate exposure data during market events

Over time, this leads to “narrative drift” where performance numbers, AUM figures, exposure data, or policy descriptions vary slightly across documents.

Small inconsistencies compound. In competitive, regulatory, or crisis-driven contexts, they matter.

The Role of Governance, Technology, and AI

As request volumes increase, many firms are turning to technology and AI-assisted drafting. But AI does not solve structural inconsistency. It amplifies it.

If the underlying data is fragmented, outdated, or duplicated, AI will reproduce those flaws at scale.

What asset managers need is a governed data foundation where:

- Approved answers are maintained centrally

- Updates are controlled and documented

- Historical responses are preserved

- Exposure and performance data are consistently reconciled

- AI tools are grounded in verified source data

In this model, AI assists with retrieval and drafting, but governance remains primary.

The shift is subtle but powerful: from manually assembling answers each time to reviewing and approving responses generated from a controlled source of truth.

From Administrative Task to Strategic Capability

In 2026, diligence response is a strategic interface between asset managers, investors, and regulators.

Firms that treat RFIs, RFPs, DDQs, 15(c) questionnaires, and event-driven requests as disconnected, reactive tasks will continue to operate under pressure.

Firms that treat them as interconnected expressions of a governed data foundation will move faster, reduce risk, and present a consistent institutional narrative even in volatile markets.

The difference is not how quickly teams type responses.

It is how deliberately they manage the information that those responses depend on.